Spanish Wealth Tax (IP) and Its Interaction with ISD: What Heirs Need to Know

How Spain's Impuesto sobre el Patrimonio applies alongside ISD — valuation overlaps, the 60% cap rule, and post-death planning for inherited assets

Author: Jacob Salama (SALAMA LEGAL SLP) | May 2025 | internationalinheritancespain.es

5/27/20264 min read

Spain's wealth tax — Impuesto sobre el Patrimonio (IP) — is a recurring annual charge on the net value of assets held by Spanish tax residents and, for non-residents, on Spanish-sited assets. Unlike most European countries which have abolished wealth taxes, Spain continues to levy IP at the state level with a minimum EUR 700,000 personal exemption and community-level modifications. From 2023, Spain's new Impuesto de Solidaridad sobre las Grandes Fortunas (ISGF) imposes a national minimum floor where communities have bonified IP to zero. Understanding IP is essential for inherited estates: valuation rules, the interaction with ISD, and planning around the 60% combined IRPF+IP cap are the key issues.

1. Wealth Tax (IP): The Framework

IP is governed by Ley 19/1991, de 6 de junio. Spanish tax residents are taxed on their worldwide net assets. Non-residents are taxed on Spanish-sited assets only. Personal exemption: EUR 700,000 at state level (communities may set higher or lower). Additional exemption: habitual residence (vivienda habitual) EUR 300,000.

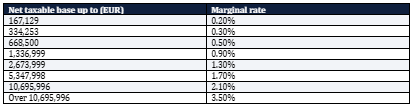

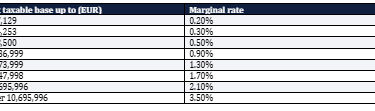

State IP rate scale (art. 30 Ley 19/1991):

Net taxable base up to (EUR)

Community variations: Madrid applies a 100% IP bonification → effective IP rate in Madrid = 0%. Andalucia since 2022 applies a 100% IP bonification → effective IP rate in Andalucia = 0%. The national ISGF floor (Ley 38/2022) means that residents in 0%-IP communities pay the ISGF at 1.7% on net assets over EUR 3M instead.

2. IP and the Inherited Estate: Post-Death Obligations

When an heir accepts an inheritance, they become the beneficial owner of the inherited assets from the date of death. Their IP declaration for the year of death must include those assets for the proportion of the year they were the owner.

IP Modelo 714 is filed annually between April and June for the previous calendar year. If the inheritance is accepted in October 2025 and the assets are worth EUR 2M, the heir includes those assets in their IP return for 2025 (filed in spring 2026), weighted for the fraction of the year (3 months out of 12 = 25% of the full-year value in the simplest approach, though Spanish practice generally uses the 31 December balance).

For non-residents inheriting Spanish assets: IP applies to Spanish-sited assets above the relevant threshold. However, if the heir is resident in Andalucia or Madrid (which have 100% IP bonifications), IP is zeroed or converted to ISGF for very large assets.

3. The 60% Cap Rule: IRPF + IP Combined Limit

Article 31 Ley 19/1991 provides that for Spanish tax residents, the combined IRPF and IP liability cannot exceed 60% of the taxpayer's IRPF taxable income for that year. If it does, IP is reduced to bring the total to 60%. However, IP cannot be reduced below 20% of its theoretical amount — a floor that prevents the cap from eliminating IP entirely.

For heirs who inherit high-value assets but have modest income: if the inherited portfolio generates low returns (e.g., property not yet rented), IP may be a significant annual cost relative to income. The 60% cap can provide relief in these cases.

4. Valuation for IP vs ISD: Same Asset, Same Value?

The valuation rules for IP and ISD use the same concept — fair market value (valor real) or, for real estate, the higher of: market value, cadastral value, or the valor de referencia (post-Ley 11/2021). For financial assets: market price on 31 December. For unquoted shares: the greater of book value and the value derived from capitalising average profits.

The IP declared value at 31 December and the ISD declared value at date of death are independent — but AEAT cross-references them. A property declared at EUR 300,000 in ISD but at EUR 500,000 in IP for the prior year (when the deceased declared it) creates a valuation inconsistency that AEAT may challenge.

5. Impuesto de Solidaridad sobre las Grandes Fortunas (ISGF)

Introduced by Ley 38/2022, de 27 de diciembre, the ISGF applies to individuals with net assets exceeding EUR 3 million. It applies regardless of whether the community has bonified IP to zero. Rate: 1.7% on EUR 3M-5M; 2.1% on EUR 5M-10M; 3.5% above EUR 10M. It is capped at 60% of IRPF income in the same way as IP.

For heirs inheriting large estates (above EUR 3M): the ISGF becomes the relevant annual tax even where IP is zero (Madrid/Andalucia). The ISGF is levied by the state — communities cannot bonify it. This was challenged before the Constitutional Court but upheld in 2024 (STC 11/2024).

6. Beckham Law and IP/ISGF

Special regime taxpayers under Art. 93 LIRPF (Beckham Law) are exempt from IP on foreign assets. They are also exempt from Modelo 720. However, following Ley 38/2022, the ISGF applies to Beckham Law taxpayers on SPANISH-sited assets above EUR 3M. Foreign assets of Beckham taxpayers are exempt from BOTH IP and ISGF during the special regime period.

For heirs who are Beckham Law taxpayers: inherited foreign assets (UK property, US securities, Israeli pension funds) are exempt from IP and ISGF while the Beckham regime applies. This makes the Beckham window valuable for structuring post-inheritance wealth before committing to ordinary Spanish residency.

LEGAL DISCLAIMER: This article is for general information only and does not constitute legal or tax advice. Tax law changes frequently. Always consult a qualified Spanish tax lawyer before taking any action. Jacob Salama (SALAMA LEGAL SLP, Colegiado no. 11.294 ICAMalaga) is a registered Spanish lawyer dedicated to private client international taxation.