Spanish Inheritance Tax for Non-Residents: Rates, Reductions and the Post-2021 Landscape

A practitioner's guide to Impuesto sobre Sucesiones y Donaciones (ISD) for heirs and beneficiaries who do not live in Spain

Author: Jacob Salama (SALAMA LEGAL SLP) | May 2025 | internationalinheritancespain.es

5/19/20266 min read

Spain's inheritance and gift tax (ISD) was for years applied more heavily to non-residents than to Spanish residents — a discrimination condemned by the European Court of Justice in the Welte case and finally remedied for all non-residents worldwide by Royal Decree-Law 17/2021. Today non-residents can access the generous regional bonifications — including Andalucia's 99% relief and EUR 1 million personal reduction — that make Spain one of the most favourable jurisdictions in Europe for family wealth transfer when the right planning is in place.

1. Legal Framework: Ley 29/1987 and the Autonomous Communities

Spanish inheritance and gift tax — Impuesto sobre Sucesiones y Donaciones — is governed at state level by Ley 29/1987, de 18 de diciembre, and its implementing Reglamento (Real Decreto 1629/1991). The state law establishes the tax base, personal reductions, rate scale and coeficientes multiplicadores. Spain's 17 autonomous communities (comunidades autónomas) have broad powers to legislate their own bonifications, surcharges and reductions — powers that most communities have exercised aggressively, resulting in vast differences in effective tax rates across the country.

For many years, non-residents were locked out of the regional legislation and subject only to the bare state tariff. The ECJ's Welte judgment (Case C-181/12, 3 September 2014) held this was an unlawful restriction on the free movement of capital under Article 63 TFEU. Spain amended its law, but initially only for EU/EEA non-residents. Royal Decree-Law 17/2021, de 14 de septiembre, extended the equal treatment to ALL non-residents regardless of nationality — expressly covering UK nationals post-Brexit, US, Israeli, and other third-country nationals.

2. Who Is Liable: Two Connecting Factors

Situation A — Worldwide estate where the deceased was habitually resident in Spain: The full worldwide estate is subject to Spanish ISD. Every asset wherever located — UK property, US securities, Swiss bank accounts, French farmhouse — falls within the Spanish ISD net. The heir's own country of residence is irrelevant to this global scope.

Situation B — Spanish-sited assets of a non-resident deceased: Even if the deceased was not a Spanish tax resident, any asset physically or legally located in Spain is subject to Spanish ISD. This includes: Spanish real estate (inmuebles), bank accounts at Spanish financial institutions, shares in Spanish companies, business assets or permanent establishments in Spain, and rights registered in Spanish public registries.

Spain has bilateral inheritance tax treaties with France (1963), Greece (1919) and Sweden (1963). With the UK, USA, Germany, Netherlands, Israel and most other countries there is no inheritance tax treaty. Both countries may tax the same asset on the same death, with limited domestic relief available under Article 23 Ley 29/1987.

3. Computing the Tax: From Gross Estate to Tax Payable

Step 1 — Gross taxable base (base imponible)

The gross taxable base is the fair market value (valor real) of all inherited assets and rights, plus the deemed capital additions prescribed by law (gifts made within 4 years of death: Art. 11 Ley 29/1987). For Spanish real estate, since 1 January 2022 the minimum taxable value is the valor de referencia published annually by the Catastro (Art. 10 Texto Refundido Ley Catastro, as amended by Ley 11/2021). Declaring below this reference value triggers automatic correction by AEAT.

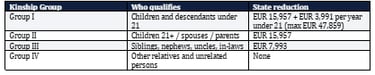

Step 2 — Personal reductions (reducciones personales)

The state law provides personal reductions that vary by kinship group. Each heir in Group I or Group II benefits from a reduction applied to their individual share. Communities with their own bonifications often provide dramatically larger reductions — Andalucia offers EUR 1,000,000 per heir for direct lineal descendants and ascendants.

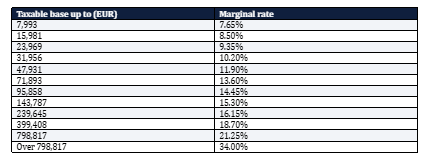

Step 3 — Rate scale (tarifa)

Step 4 — Coeficiente multiplicador

The gross tax (cuota íntegra) is multiplied by a coeficiente based on the heir's kinship group and their pre-existing wealth. Groups I and II with pre-existing wealth below EUR 402,678 apply a multiplier of 1.0 — no surcharge. Group IV (unrelated persons) apply a multiplier of 2.0 at minimum, doubling the state tariff.

4. Regional Bonifications: The Critical Differences

Andalucia — 99% bonification + EUR 1M personal reduction

Decreto Legislativo 1/2018 of Andalucia: Groups I and II benefit from a personal reduction of EUR 1,000,000 per heir and a 99% bonification on the remaining cuota íntegra. A child inheriting EUR 900,000 in Andalucia pays effectively zero ISD. Even an estate of EUR 5 million distributed among two children is taxed at under 1% of effective value.

Madrid — 99% bonification

Community of Madrid: Ley 7/2017 provides a 99% bonification for Groups I and II. No special additional personal reduction beyond the state amount, but the 99% bonification renders ISD near-zero for direct family.

Cataluña — Complex and less generous

Cataluña's rules are the most complex and least generous for non-residents. The group reductions are structured differently, the bonification is partial, and effective rates of 7-10% on large inheritances are common. Professional advice is essential.

Comunidad Valenciana — 75% bonification

Valencia: 75% bonification for Groups I and II under Art. 12 Ley 13/1997. Effective rate approximately 5-7% for direct heirs on a EUR 500,000 estate.

Galicia — 99% bonification

Galicia mirrors the Andalucia/Madrid approach: 99% bonification for Groups I and II, with a EUR 400,000 personal reduction.

5. How Non-Residents Choose Which Region's Rules Apply

Post Royal Decree-Law 17/2021, the rules are:

Where there are Spanish immovable assets: apply the rules of the autonomous community where the greatest value of Spanish immovable property is located.

No Spanish immovable assets: apply the rules of the autonomous community where the deceased was last habitually resident in Spain.

Where the deceased was never habitually resident in Spain and there are no Spanish immovable assets: apply the state rules (least favourable).

Practical consequence: a British heir inheriting a Malaga flat worth EUR 800,000 from a Malaga-resident parent automatically benefits from Andalucia's 99% bonification and EUR 1M personal reduction — irrespective of where the heir lives.

6. Deadlines, Filing and Common Errors

6-month filing deadline: The ISD return must be filed within 6 months of the date of death (Art. 67 RD 1629/1991). Late filing triggers surcharges of 5% (first 3 months), 10% (3-6 months), 15% (6-12 months) or 20% (over 12 months), plus late payment interest at 3.75% annually.

Prorroga (extension): A single 6-month extension may be requested via the competent regional tax authority — but ONLY within the initial 6-month window. Once expired, it cannot be requested. Many heirs miss this.

Where to file: Assets in Andalucia → Agencia Tributaria de Andalucia. Assets in Madrid → Comunidad de Madrid tax authority. Each autonomous community has its own administration. Non-residents must appoint a fiscal representative in Spain.

COMMON ERROR: Undervaluing property below the valor de referencia — triggers automatic AEAT correction plus surcharges.

COMMON ERROR: Missing the prorroga window — requesting after 6 months when it is no longer available.

COMMON ERROR: Not including Spanish bank accounts or life insurance as part of the estate.

COMMON ERROR: Applying the wrong autonomous community — e.g. applying state rules when Andalucia would provide 99% relief.

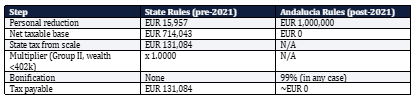

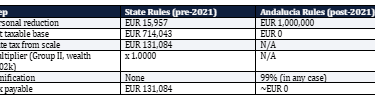

7. Worked Example: Non-Resident Heir, Malaga Estate

Facts: James (UK resident, British national) inherits from his mother Carmen (habitually resident in Malaga). Estate: apartment EUR 650,000 + bank account EUR 80,000 = EUR 730,000. No mortgage. James is Group II (adult child). No pre-existing wealth in Spain.

Saving: EUR 131,084. This is the practical importance of RD-L 17/2021 for non-resident heirs.

Key Links

AEAT — Spanish Tax Agency: https://www.agenciatributaria.es

BOE — Official State Gazette: https://www.boe.es

EU Succession Regulation 650/2012: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32012R0650

OECD — Tax Treaties and CRS: https://www.oecd.org/tax/treaties/

Spanish Ministry of Finance: https://www.hacienda.gob.es

International Inheritance Spain: https://www.internationalinheritancespain.es

International Taxation Spain: https://www.internationaltaxationspain.com

Real Estate Lawyer Costa del Sol: https://www.realestatelawyercostadelsol.com

Tourist Licence Andalucia: https://www.licenciaturisticaandalucia.es

LEGAL DISCLAIMER: This article is for general information only and does not constitute legal or tax advice. Tax law changes frequently. Always consult a qualified Spanish tax lawyer before taking any action. Jacob Salama (SALAMA LEGAL SLP, Colegiado no. 11.294 ICAMalaga) is a registered Spanish lawyer dedicated to private client international taxation.