Selling an Inherited Spanish Property: IRPF, Plusvalía Municipal and the 3% Withholding Explained

The three tax layers that apply when heirs sell a property inherited in Spain — and how to calculate and minimise each one

Author: Jacob Salama (SALAMA LEGAL SLP) | May 2025 | internationalinheritancespain.es

5/25/20265 min read

Selling an inherited Spanish property creates at least three distinct tax obligations: a capital gains charge under IRPF or IRNR, a Plusvalía Municipal levied by the local Ayuntamiento, and — for non-residents — a 3% retention withheld at source by the buyer. Understanding how each layer works, how the acquisition cost is determined by reference to the ISD return, and what planning can legitimately reduce the total bill is essential for any heir considering a sale.

1. Layer 1: Capital Gains Tax — IRPF (Residents) or IRNR (Non-Residents)

Acquisition cost for ISD heirs: Article 36 LIRPF

For a property inherited rather than purchased, the acquisition cost is defined by Article 36 Ley 35/2006 (LIRPF) as: (i) the value declared in the ISD return (valor declarado en el ISD), plus (ii) ISD actually paid attributable to that asset, plus (iii) acquisition expenses paid by the heir: notary fees for the escritura de adjudicación, Land Registry inscription fees, and professional fees directly connected to the acquisition.

This definition is highly favourable: if the ISD value was high (e.g. where no Andalucia bonification was available and full ISD was paid), the high ISD value is 'stepped up' into the acquisition cost, reducing the future IRPF gain. Conversely, if the property was inherited under Andalucia's 99% bonification (with effectively zero ISD paid), the acquisition cost is the declared value alone, without any ISD add-back.

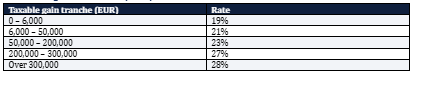

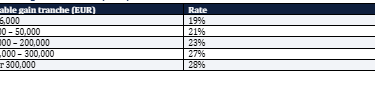

IRPF savings income rates (2025)

Taxable gain tranche (EUR)

Rate

IRNR — Non-Resident Income Tax

For a non-resident heir selling a Spanish property, the charge falls under Real Decreto Legislativo 5/2004 (LIRNR). The capital gain is the same calculation as IRPF but the rate is flat:

EU and EEA residents: 19% flat rate

UK nationals (post-Brexit): 19% rate, per RD-L 3/2020 maintaining EU national treatment for capital gains pending full legislative alignment. Confirm current rate with a tax adviser.

US, Israeli and other third-country nationals: 24% flat rate

2. The 3% Withholding at Source (Retención IRNR)

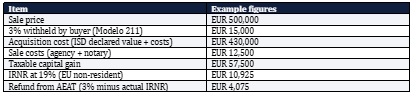

Article 25.2 LIRNR requires the buyer of a Spanish property from a non-resident seller to withhold 3% of the agreed sale price and pay it to AEAT within one month of the sale (Modelo 211). This is a payment on account of the non-resident seller's IRNR liability — not a final tax.

The seller then files Modelo 210 within 3 months of the sale date, declaring the actual capital gain and computing the true IRNR liability. If the 3% withholding exceeds the actual tax, AEAT refunds the difference. AEAT typically processes IRNR refunds within 6-18 months of filing.

Item

3. Layer 2: Plusvalía Municipal (IIVTNU)

The Impuesto sobre el Incremento de Valor de los Terrenos de Naturaleza Urbana (IIVTNU) is a municipal tax on the theoretical increase in the cadastral value of the land component of an urban property. It is payable to the Ayuntamiento within 30 days of the sale (for sales; 6 months for inheritances).

Following the landmark Constitutional Court ruling STC 182/2021 (26 October 2021) and the subsequent Royal Decree-Law 26/2021, taxpayers now have a choice of two calculation methods:

Objective method: Cadastral land value at sale date × annual coefficient (set by each municipality within MINHAC-approved maximums) × number of full years held (capped at 20). The coefficients for 2025 are updated annually. This is the default and simpler approach.

Real increase method: Actual increase in land value = (sale price × land proportion at sale) minus (acquisition price × land proportion at acquisition). Requires certified appraisals if the figures cannot be derived from documented transaction prices. Useful where the land has barely appreciated or where the objective method produces a higher result.

Post-STC 182/2021: if there is no actual increase in land value — demonstrated with documentary evidence — Plusvalía Municipal is zero. The Ayuntamiento may challenge the evidence. Expert appraisal (informe de tasación) is recommended.

4. Coordinating the Three Tax Layers

The total tax cost of a sale must be computed across all three layers before deciding to sell. Practical considerations:

Time of sale post-inheritance: selling within 1 year of inheriting is taxed the same as selling after 5 years for IRPF purposes — there is no longer a holding period reduction in Spain (the corrección monetaria was abolished for real estate in 2015).

ISD step-up: if the heir paid significant ISD on the property, the full ISD payment is added to the acquisition cost, reducing the IRPF/IRNR gain. In some cases — particularly pre-2021 non-residents who paid full state ISD rates — this can dramatically reduce or eliminate the IRPF gain.

Community-level Plusvalía: rates vary significantly between municipalities. Central Madrid, Barcelona and prime coastal areas often have the highest coefficients and cadastral values.

5. Reinvestment Exemption: What the Heir Cannot Claim

Article 38.1 LIRPF provides that a capital gain on sale of the habitual residence (vivienda habitual) is exempt if the full proceeds are reinvested in a new habitual residence within 2 years. This exemption is frequently misunderstood by heirs. It requires: (a) the property sold was the seller's own habitual residence for at least 3 years; and (b) the proceeds are reinvested in the seller's own new habitual residence.

An heir who inherited a property that was the deceased parent's home — but not the heir's own habitual residence — cannot claim this exemption. AEAT audits regularly disclose attempted improper claims of this exemption by heirs.

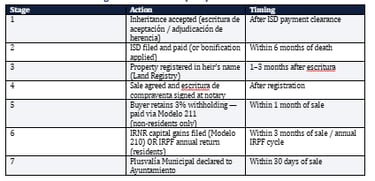

6. Timeline for Selling an Inherited Property

Stage

Action

Timing

7. Common Planning Points

Pre-sale ISD compliance check: Verify the ISD return was filed correctly and the valor de referencia was respected. AEAT cross-checks IRPF acquisition cost against ISD records.

Co-ownership sales: Where multiple heirs own the property jointly, each must file their own IRPF/IRNR return for their proportionate gain. Coordinate filing to avoid conflicting declared values.

Currency gains for non-euro transactions: If the original ISD value was in a non-euro currency, conversion at the relevant rate at each date of acquisition and sale creates additional complexity. Document the exchange rates used.

Loss positions: If the property is sold at a loss (valor de venta < acquisition cost), the capital loss can be offset against other capital gains in the same IRPF return or carried forward for 4 years.

Key Links

AEAT — Spanish Tax Agency: https://www.agenciatributaria.es

BOE — Official State Gazette: https://www.boe.es

EU Succession Regulation 650/2012: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32012R0650

OECD — Tax Treaties and CRS: https://www.oecd.org/tax/treaties/

Spanish Ministry of Finance: https://www.hacienda.gob.es

International Inheritance Spain: https://www.internationalinheritancespain.es

International Taxation Spain: https://www.internationaltaxationspain.com

Real Estate Lawyer Costa del Sol: https://www.realestatelawyercostadelsol.com

Tourist Licence Andalucia: https://www.licenciaturisticaandalucia.es

LEGAL DISCLAIMER: This article is for general information only and does not constitute legal or tax advice. Tax law changes frequently. Always consult a qualified Spanish tax lawyer before taking any action. Jacob Salama (SALAMA LEGAL SLP, Colegiado no. 11.294 ICAMalaga) is a registered Spanish lawyer dedicated to private client international taxation.