Gift vs Inheritance in Spain: Planning the Transfer of Wealth Tax-Efficiently

When lifetime gifts are more tax-efficient than bequests — and when they are not — with worked examples for Spanish and non-Spanish residents

Author: Jacob Salama (SALAMA LEGAL SLP) | May 2026 | internationalinheritancespain.es

6/1/20264 min read

In jurisdictions such as the UK and USA, lifetime gifts are frequently the cornerstone of intergenerational wealth planning. In Spain, ISD applies to both inheritances and gifts — but the rules on which region's law applies differ sharply between the two. In many cases, a lifetime gift is subject to far less generous regional bonifications than a bequest at death, producing counter-intuitive results. This guide compares the two routes systematically and identifies the key planning decisions.

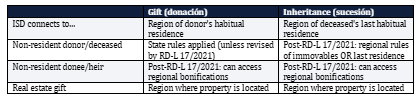

1. ISD: Same Tax, Different Connecting Rules for Gifts and Inheritances

Ley 29/1987 governs both gifts (donaciones) and inheritances (sucesiones). The tax base and rate structure are broadly the same, but the regional connecting rules differ significantly:

Key consequence: if a non-resident parent in the UK gifts a Malaga flat to their non-resident UK-based child, the gift connects to the UK (donor's habitual residence). The UK has no gift tax. However, the Spanish property aspect creates a Spanish ISD event connecting to the region where the immovable is — Andalucia. Both parties being non-resident, the post-2021 rules apply.

2. When Gifts are Tax-Efficient in Spain

Gifts of Spanish real estate within Andalucia — donor and donee: near-zero ISD

If both donor and donee are habitually resident in Andalucia, a gift of real estate benefits from the Andalucia bonification (99%) and the EUR 1M personal reduction per donee. The ISD on a EUR 800,000 gift of Andalucia real estate from parent to adult child is approximately zero.

Pre-immigration gifts to non-Spanish family members

A parent planning to move to Spain under the Beckham Law may consider gifting high-value assets to children before establishing Spanish residency. Pre-immigration gifts are governed by the home-country law (e.g., UK PETs or US annual exclusion gifts), not Spanish ISD, provided the donor is not yet habitually resident in Spain.

3. When Inheritances Are More Tax-Efficient Than Gifts

ISD step-up in acquisition cost for IRPF purposes

When an asset is inherited, the heir's acquisition cost for IRPF (capital gains) is the ISD declared value. If the asset has appreciated significantly during the parent's lifetime, inheriting provides a step-up in cost basis that a lifetime gift does not.

Example: Parent purchased a Malaga flat in 2005 for EUR 200,000. Current value: EUR 700,000. IRPF gain if parent sells: EUR 500,000 (taxed at up to 28%). If parent gifts the flat: recipient's acquisition cost is EUR 700,000 (ISD value) — but the parent is treated as having disposed of it for EUR 700,000, generating the same EUR 500,000 IRPF gain. If parent dies holding the flat: heir's acquisition cost = EUR 700,000 (ISD value). The EUR 500,000 gain disappears — it is never subject to IRPF. This is the 'step-up on death' benefit that makes bequests attractive for highly appreciated assets.

Life insurance written in trust vs at death

Life insurance proceeds paid on death and received by named beneficiaries under Art. 3.1.c Ley 29/1987 are subject to ISD. However, the ISD treatment is often more favourable than an inter vivos gift of equivalent value — particularly in regions with 99% bonifications. The EUR 9,195 state reduction for life insurance for Group I and II beneficiaries is a baseline reduction; communities often provide more.

4. The IRPF Disposal Problem for Lifetime Gifts

Article 33.3 LIRPF provides that a gift (donación) does not generate an IRPF capital gain for the donor — with ONE exception: lucrative inter vivos disposals of assets where the donor's acquisition cost exceeds the ISD value are treated as a disposal at fair market value. This means the donor is taxed on the full unrealised gain at the time of the gift, even though they received no proceeds.

Practical consequence: gifting a property with significant latent gain to a child is a taxable IRPF event for the Spanish-resident donor. The gain is real even if no cash is received. Death, by contrast, does not trigger an IRPF disposal — the gain disappears permanently. This is a major reason why holding appreciated assets until death is often preferable to making lifetime gifts.

5. Gifts of Non-Spanish Assets: The International Dimension

A Spanish-resident parent gifting foreign assets (e.g., UK shares, US securities, French property) to a Spanish-resident child: the gift connects to the donor's habitual residence (Spain) for ISD purposes. The regional bonification of the donor's autonomous community applies.

A Spanish-resident parent gifting foreign assets to a non-resident child: post-RD-L 17/2021, the donee can access the regional bonifications of the donor's community. In Andalucia or Madrid: near-zero ISD even for gifts of foreign assets.

A non-resident parent gifting Spanish real estate to a non-resident child: Spanish ISD applies to the property (as a Spanish-sited asset). Post-2021, regional bonification rules apply — Andalucia's 99% bonification is available for this transaction.

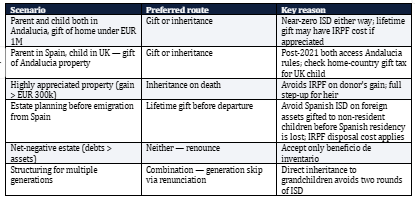

6. Decision Matrix: Gift vs Inheritance

Scenario

Preferred route

Key reason

7. Succession Pacts (Pactos Sucesorios)

In Cataluña, the Balearic Islands, Galicia, Aragon and the Basque Country, civil law allows succession pacts (pactos sucesorios) — contractual arrangements governing future inheritance. Under Article 33.3.b LIRPF and DGT rulings, the transfer under a pacto sucesorio is treated as an inheritance (succesión), NOT as a lifetime gift, for ISD purposes. This means the transferee gets the regional bonification applicable on death and — critically — the ISD value becomes the acquisition cost for IRPF without any IRPF disposal charge on the transferor. A powerful tool where the applicable regional civil law permits it.

Key Links

AEAT — Spanish Tax Agency: https://www.agenciatributaria.es

BOE — Official State Gazette: https://www.boe.es

EU Succession Regulation 650/2012: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32012R0650

OECD — Tax Treaties and CRS: https://www.oecd.org/tax/treaties/

Spanish Ministry of Finance: https://www.hacienda.gob.es

International Inheritance Spain: https://www.internationalinheritancespain.es

International Taxation Spain: https://www.internationaltaxationspain.com

Real Estate Lawyer Costa del Sol: https://www.realestatelawyercostadelsol.com

Tourist Licence Andalucia: https://www.licenciaturisticaandalucia.es

LEGAL DISCLAIMER: This article is for general information only and does not constitute legal or tax advice. Tax law changes frequently. Always consult a qualified Spanish tax lawyer before taking any action. Jacob Salama (SALAMA LEGAL SLP, Colegiado no. 11.294 ICAMalaga) is a registered Spanish lawyer dedicated to private client international taxation.